Financial Validation Rules for Face Amount and Premium Affordability

Financial validation helps determine the maximum death benefit and premium an applicant may qualify for, allowing potential financial suitability issues to be identified and corrected before the application reaches the carrier. Based on an audit of 2,000 recent applications, approximately 3% would not have met these validation requirements, highlighting the importance of addressing financial suitability early in the application process.

Alert #1: Death Benefit Justification

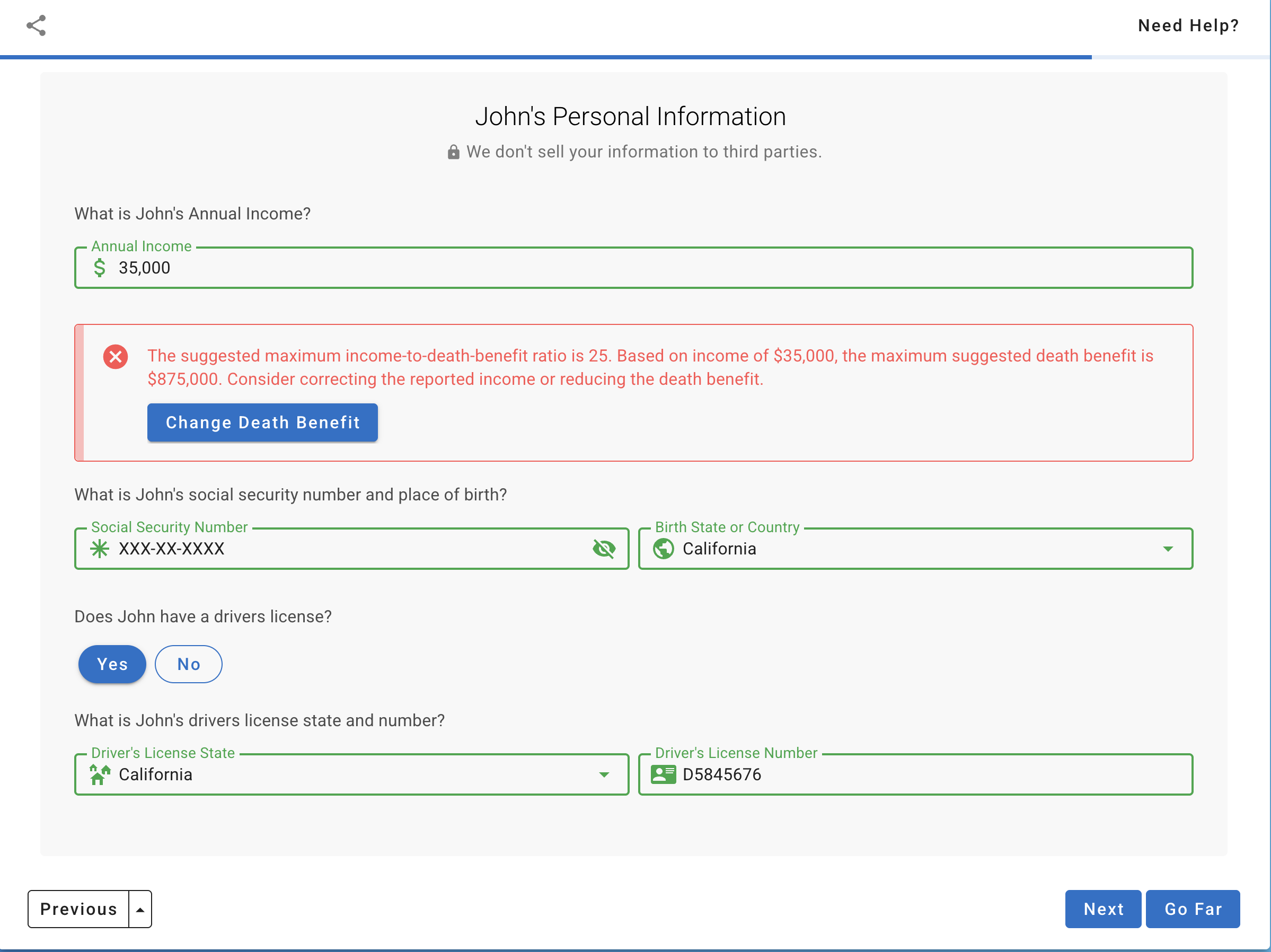

This alert evaluates whether the requested death benefit is reasonable relative to the insured’s income. For insureds age 18 and older, we compare the requested death benefit against an age-based multiple of annual income.

Suggested Maximum Death Benefit Multiples

| Age | Suggested Maximum Death Benefit |

|---|---|

| 18–40 | 35× annual income |

| 41–50 | 25× annual income |

| 51–60 | 20× annual income |

| 61+ | 15× annual income |

This alert is not triggered for:

- Guaranteed issue products

- Homemakers

- Students

- Policies with a collateral assignee

The alert is also suppressed when the insured’s liabilities or net worth support the total amount of insurance in force, including any active existing coverage.

Alert #2: Premium Affordability

This alert evaluates whether the policy premium is affordable based on the insured’s income.

Maximum Premium-to-Income Ratios

| Annual Income | Maximum Premium Ratio |

|---|---|

| Under $50,000 | 10% |

| $50,000–$99,999 | 15% |

| $100,000–$249,999 | 20% |

| $250,000 and above | 25% |

The premium is also considered acceptable if it does not exceed 3% of the applicant’s assets or net worth, depending on the financial information collected during the application process.

Limited-Pay Policies

For limited-pay policies, premiums are levelized as though they were paid through age 100 to ensure a consistent affordability assessment.